The search for real estate loans in Costa Rica is grabbing attention from expats and investors everywhere. Here is the surprise. Foreign buyers are routinely required to put down 30 to 50 percent of the property value, a much steeper upfront cost than what most expect from North American or European banks. Most people think bank mortgages are the only path to financing, but in Costa Rica, alternatives like seller financing or private lending can actually speed up the buying process and offer a totally different set of rules. Get ready to discover why stricter rules and unique options are reshaping what it means to invest in Costa Rican property.

Table of Contents

- Understanding Real Estate Loan Basics In Costa Rica

- Popular Types Of Real Estate Loans For Expats And Investors

- How To Choose The Right Loan For Your Investment Goals

- Essential Tips For Securing Real Estate Loans As A Foreigner

Quick Summary

| Takeaway | Explanation |

|---|---|

| Higher Down Payments Required | Foreign investors in Costa Rica typically face down payment requirements ranging from 30% to 50% of the property value, significantly higher than many North American markets. |

| Interest Rates and Loan Terms | Interest rates for loans can range from 6% to 16%, with terms usually spanning from 3 to 25 years depending on the loan type, affecting overall investment returns. |

| Comprehensive Documentation Needed | Investors must prepare extensive financial documentation, including proof of income, credit history, and professional translations into Spanish, to meet stringent lending requirements. |

| Legal Expertise is Crucial | Working with local legal professionals is essential to navigate complex regulations and ensure compliance throughout the loan process and property acquisition. |

| Flexible Financing Options Available | Alternatives like seller financing and private lending may offer more adaptable terms, providing opportunities for quicker transactions compared to traditional bank mortgages. |

Understanding Real Estate Loan Basics in Costa Rica

Navigating the real estate loan landscape in Costa Rica requires understanding unique local financial dynamics that differ significantly from traditional lending markets. Foreign investors and expats face distinctive challenges when seeking property financing, making comprehensive knowledge crucial for successful real estate transactions.

The Costa Rican Real Estate Financing Ecosystem

Real estate loans in Costa Rica operate within a complex framework that prioritizes local economic regulations and risk management. Unlike many North American markets, Costa Rican lenders approach property financing with more stringent requirements designed to protect both borrowers and financial institutions. Foreign investors typically encounter more restrictive lending standards that demand higher down payments and more comprehensive documentation.

Most private lenders and financial institutions in Costa Rica require substantial proof of income, excellent credit history, and significant upfront capital. Foreign borrowers often need to demonstrate stable international income sources, typically through bank statements, tax returns, and employment verification. The average down payment for foreign investors ranges between 30% to 50% of the total property value, substantially higher than traditional mortgage requirements in the United States or Canada.

Loan Structure and Key Considerations

The loan structures in Costa Rica are characterized by shorter repayment terms and higher interest rates compared to more established real estate markets. Interest rates for foreign investors typically range from 7% to 12% annually, reflecting the perceived higher risk associated with international borrowers. Loan terms generally span 5 to 15 years, with most private lenders preferring shorter durations to minimize long term financial exposure.

Legal documentation plays a critical role in Costa Rican real estate financing. Every loan transaction requires meticulous legal verification, including property title searches, comprehensive risk assessments, and formal mortgage registrations. Investors must work with local legal professionals who understand the intricacies of Costa Rican property law to ensure smooth and legally compliant transactions.

Foreign investors should also be aware of unique local financing options. Learn more about private lending strategies that can provide alternative pathways to property acquisition. Seller financing, for instance, remains a popular alternative to traditional bank loans, offering more flexible terms and faster transaction processes.

Key financial considerations for real estate loans in Costa Rica include:

- Currency Risks: Most loans are denominated in US dollars to mitigate exchange rate fluctuations

- Property Valuation: Comprehensive independent appraisals are mandatory for loan approval

- Legal Compliance: Strict adherence to local banking regulations and foreign investment laws

Successful real estate investment in Costa Rica demands a nuanced understanding of local financial ecosystems. Investors must approach loan acquisition with patience, thorough research, and a willingness to adapt to unique local requirements. By preparing comprehensive financial documentation, understanding local lending practices, and working with experienced local professionals, foreign investors can effectively navigate the complex world of Costa Rican real estate financing.

The journey to securing a real estate loan in Costa Rica is not simply about finding funding but about building a strategic approach that aligns with local economic frameworks and investment opportunities.

Popular Types of Real Estate Loans for Expats and Investors

Real estate loans in Costa Rica offer diverse financing options tailored to meet the unique needs of expats and international investors. Understanding these loan types is crucial for making informed investment decisions in this dynamic property market.

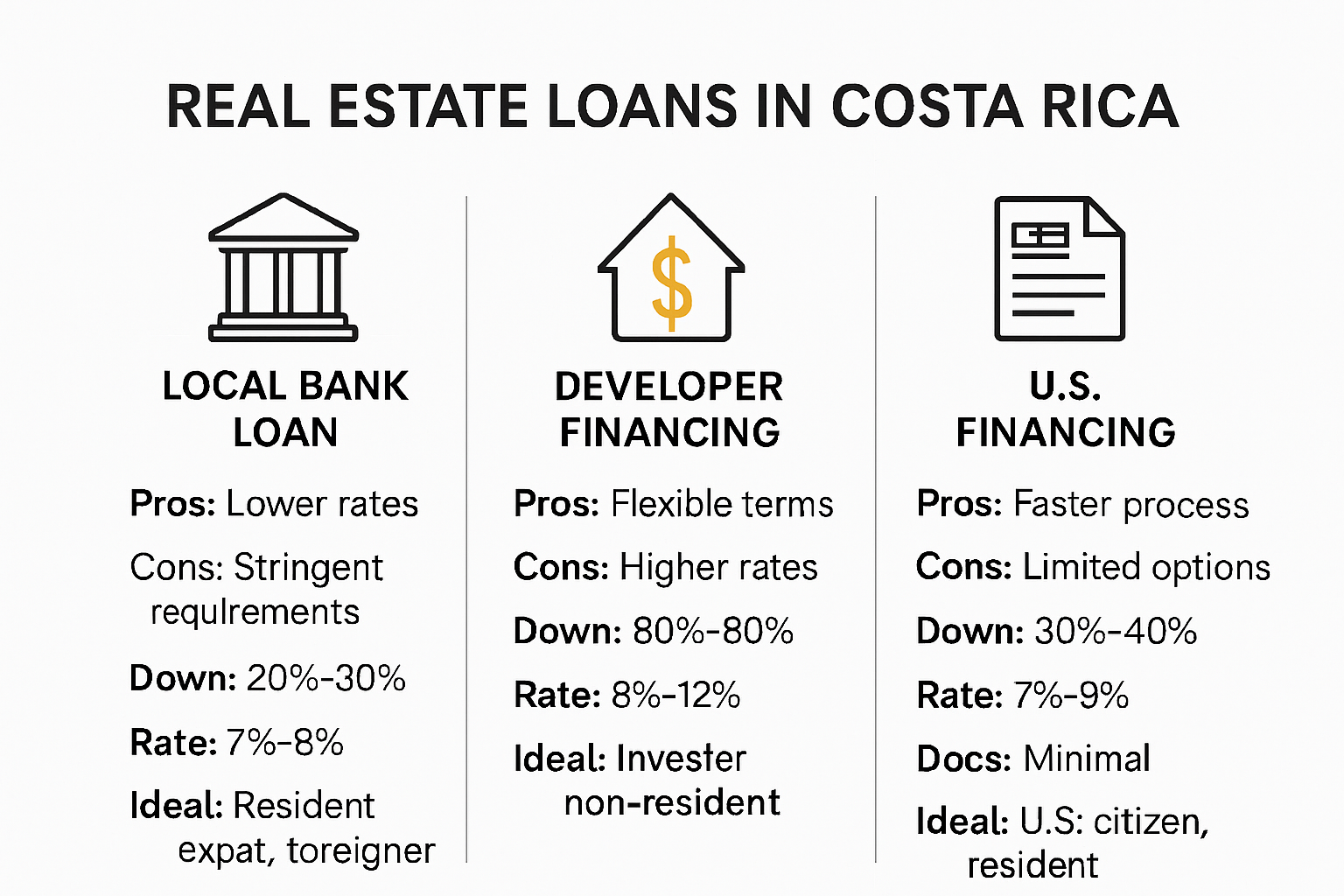

Local Bank Mortgages: Traditional Financing Pathway

Local bank mortgages represent the most conventional financing method for real estate purchases in Costa Rica. These loans typically require substantial documentation and stringent approval processes. Foreign investors can access these mortgages, but they face more complex qualification criteria compared to local residents.

Bank mortgage characteristics include strict income verification, comprehensive credit checks, and significant down payment requirements. Most local banks demand down payments ranging from 30% to 50% of the property’s total value for foreign investors. Interest rates fluctuate between 7% and 9.5% annually, with loan terms extending from 15 to 25 years. Foreign borrowers must provide extensive documentation, including international income statements, tax returns, and proof of financial stability.

Seller Financing: Flexible Alternative to Traditional Loans

Seller financing emerges as a popular and flexible option for expats seeking property acquisition in Costa Rica. This financing method allows direct negotiation between the property seller and buyer, bypassing traditional banking institutions. Explore strategic investment approaches that can maximize your financial potential.

Seller financing typically features more adaptable terms compared to bank mortgages. Down payments usually range from 30% to 50%, with interest rates between 6% and 8%. Loan terms are generally shorter, spanning 3 to 5 years, providing faster property transfer and reduced long term financial commitment. This approach offers significant advantages for investors seeking quicker transactions and more personalized financing arrangements.

Private Lending and Developer Financing: Specialized Investment Strategies

Private lending and developer financing represent innovative approaches to real estate loans in Costa Rica. These options cater specifically to investors seeking alternative funding mechanisms. Private lenders often provide more flexible terms, with interest rates ranging from 12% to 16% and potential down payments up to 70% of the property value.

Developer financing presents another strategic option, particularly for new construction projects. These loans typically feature interest rates between 8% and 12%, with down payments ranging from 20% to 30%. The specific terms depend on individual development projects and the developer’s financial structure.

Key considerations for expats and investors selecting real estate loans in Costa Rica include:

- Comprehensive Documentation: Prepare extensive financial records

- Currency Stability: Understand loan denominations and exchange rate risks

- Legal Compliance: Work with local legal professionals to navigate complex regulations

Successful real estate investment in Costa Rica requires a nuanced understanding of available financing options. Investors must carefully evaluate each loan type, considering their individual financial goals, risk tolerance, and long term investment strategies. By thoroughly researching and comparing different loan structures, expats can identify the most suitable financing approach for their specific property investment needs.

The Costa Rican real estate market offers multiple pathways to property ownership, each with unique advantages and considerations. Thorough preparation and strategic financial planning are essential for navigating these diverse loan options effectively.

How to Choose the Right Loan for Your Investment Goals

Selecting the ideal real estate loan in Costa Rica requires a strategic approach that aligns with your specific investment objectives, financial capacity, and long term property goals. Investors must carefully evaluate multiple factors to ensure their financing strategy supports their broader investment vision.

Assessing Your Investment Profile and Financial Capacity

Choosing the right loan begins with a comprehensive assessment of your individual investment profile. Foreign investors must conduct a thorough self evaluation of their financial strengths, risk tolerance, and investment timelines. This involves analyzing personal income streams, existing assets, credit history, and long term financial objectives.

Key considerations include understanding your cash flow, determining the maximum monthly mortgage payment you can comfortably sustain, and evaluating your ability to meet down payment requirements. Different loan types demand varying levels of financial commitment. Local bank mortgages typically require more substantial upfront capital and stringent financial documentation, while seller financing might offer more flexible terms for investors with diverse financial backgrounds.

Matching Loan Structures to Investment Strategies

Each loan type presents unique advantages aligned with specific investment strategies. Short term investors might prefer seller financing with its flexible 3 to 5 year terms, while long term property holders could benefit from traditional bank mortgages offering extended 15 to 25 year repayment schedules. Explore strategic investment approaches that can help you optimize your financial planning.

Investors focused on rental income should calculate potential revenue against loan expenses, ensuring the property generates sufficient cash flow to cover mortgage payments. Those planning property development might find developer financing more suitable, with terms specifically designed for construction and renovation projects. Private lending options provide additional flexibility for investors seeking alternative financing mechanisms.

Evaluating Risk and Long Term Financial Impact

Comprehensive risk assessment is crucial when selecting a real estate loan in Costa Rica. Investors must consider multiple financial variables including interest rates, currency exchange risks, and potential market fluctuations. Interest rates ranging from 6% to 16% across different loan types can significantly impact overall investment returns.

Currency denomination represents another critical risk factor. Most loans in Costa Rica are structured in US dollars to mitigate exchange rate volatility. Investors must carefully analyze potential currency fluctuations and their potential impact on loan repayment capabilities.

Key decision making factors include:

- Income Stability: Consistent and verifiable international income

- Risk Tolerance: Ability to manage potential financial uncertainties

- Investment Timeline: Short term versus long term property objectives

Successful real estate investment in Costa Rica demands a holistic approach that balances financial capabilities, investment goals, and risk management. Investors should consult with local financial advisors, real estate professionals, and legal experts to develop a comprehensive loan strategy tailored to their unique circumstances.

Ultimately, choosing the right real estate loan is about creating a financial framework that supports your broader investment vision while providing flexibility and protecting your financial interests in the dynamic Costa Rican property market.

Essential Tips for Securing Real Estate Loans as a Foreigner

Securing a real estate loan in Costa Rica as a foreign investor requires strategic preparation, comprehensive documentation, and a nuanced understanding of local financial regulations. Foreign borrowers must navigate a complex landscape of legal requirements, financial scrutiny, and specialized lending practices unique to the Costa Rican market.

Comprehensive Financial Documentation Preparation

Successful loan acquisition begins with meticulous financial documentation. Foreign investors must compile an extensive portfolio of financial records that demonstrate economic stability and reliable income sources. This documentation typically includes international bank statements, tax returns from the past three years, proof of employment or business ownership, and comprehensive income verification from multiple sources.

Translation becomes a critical component of the documentation process. All financial documents must be professionally translated into Spanish and authenticated by certified legal professionals. This requirement adds complexity to the loan application process, necessitating additional time and financial investment. Investors should budget for professional translation services and legal verification to ensure smooth documentation submission.

Understanding Lending Requirements and Financial Expectations

Costa Rican lenders impose significantly more stringent requirements on foreign borrowers compared to local residents. Down payment expectations typically range from 30% to 50% of the total property value, substantially higher than traditional mortgage requirements in many other countries. Interest rates for foreign investors usually fluctuate between 7% and 12% annually, reflecting the perceived increased financial risk.

Discover advanced lending strategies that can help you navigate the complex financial landscape. Investors must demonstrate robust financial health through multiple verification channels. This includes maintaining substantial liquid assets, showing consistent income streams, and providing comprehensive credit history documentation from their home country.

Navigating Legal and Regulatory Complexities

Foreign real estate loan applications in Costa Rica involve intricate legal and regulatory processes. Investors must work closely with local legal professionals who specialize in international property transactions. These experts help navigate the complex documentation requirements, ensure compliance with local financial regulations, and provide critical guidance throughout the loan acquisition process.

Key legal considerations include verifying property titles, understanding local ownership restrictions, and ensuring all financial transactions comply with Costa Rican banking regulations. Foreign investors should be prepared for potentially lengthy approval processes that can extend several months, requiring significant patience and financial planning.

Critical strategies for foreign investors include:

- Financial Transparency: Provide complete and verifiable financial documentation

- Professional Support: Engage local legal and financial experts

- Comprehensive Preparation: Understand and anticipate extensive documentation requirements

Successful loan acquisition demands a holistic approach that combines thorough financial preparation, legal expertise, and a deep understanding of Costa Rican lending practices. Foreign investors must view the loan application process as a comprehensive journey requiring strategic planning, patience, and professional guidance.

Ultimately, securing a real estate loan in Costa Rica as a foreigner is about demonstrating financial reliability, understanding local regulatory frameworks, and presenting a compelling investment profile that mitigates perceived financial risks. Preparation, transparency, and professional support are the cornerstones of a successful loan application strategy.

Frequently Asked Questions

What types of real estate loans are available for expats in Costa Rica?

In Costa Rica, expats can access various real estate loans, including local bank mortgages, seller financing, and private lending. Each option has unique requirements and terms, allowing buyers to choose the best fit for their financial situation.

How much of a down payment do I need for a mortgage in Costa Rica?

Foreign buyers typically need to make a down payment ranging from 30% to 50% of the property value when seeking a mortgage in Costa Rica. This requirement is higher compared to many North American markets.

What documentation is required to secure a real estate loan as a foreigner in Costa Rica?

Foreign investors must prepare comprehensive financial documentation, including proof of income, credit history, and documentation translated into Spanish. This may include international bank statements, tax returns, and verification of employment or business ownership.

What are the interest rates for real estate loans in Costa Rica?

Interest rates for real estate loans in Costa Rica generally range from 6% to 16%, depending on the loan type. Rates can vary based on the lender’s assessment of risk and the borrower’s financial profile.

Ready for Flexible Real Estate Financing in Costa Rica?

Are you tired of hitting roadblocks like high down payments, slow approvals, and piles of documentation when you try to secure a real estate loan as an expat or investor in Costa Rica? This article highlights how traditional banks ask for 30-50 percent down and put you through a maze of paperwork. But you do not have to let these challenges stop your property dreams. CostaRicaLoanExperts.net offers a smarter, faster way to unlock property financing with private, collateral-backed loans tailored for international buyers, entrepreneurs, and locals who need flexibility and speed.

Break free from rigid restrictions. Tap into solutions built just for your needs. Discover how our private lending platform can help you overcome strict lending requirements, access funds quickly, and take advantage of investment loans that match your goals. Visit CostaRicaLoanExperts.net now to connect with trusted lenders, start your application, or learn how you can secure high-yield, real estate-backed investments in Costa Rica. Take your next step today while opportunities are on your side.