Expat property financing is shifting fast. Banks now ask expats for down payments as high as 50 percent of a property’s value. Most people expect getting a loan abroad to be all about credit scores and paperwork. That barely scratches the surface. The real surprise is how the smartest strategies this year rely on alternative lenders and legal insights most investors overlook. Curious why so many expats are unlocking global real estate while others hit roadblocks? Here is what actually matters in 2025.

Table of Contents

- Key Expat Property Financing Options Explained

- Eligibility, Documentation, And Local Regulations

- Maximizing Passive Income With Global Property

- Common Challenges And Expert Solutions

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand Financing Options | Explore traditional banking, private lending, and developer financing as key pathways for expat property purchases, each with its unique advantages and challenges. |

| Prepare Comprehensive Documentation | Gather extensive documentation, including income verification, legal status, and bank statements, to meet lender requirements and streamline approvals. |

| Navigate Local Regulations | Engage with local legal experts to understand property ownership laws, tax implications, and foreign investment restrictions that could affect your investment. |

| Maximize Passive Income Strategies | Consider strategies like rental property investments, Real Estate Investment Trusts (REITs), and collaborative investment models for generating passive income. |

| Implement Risk Mitigation Measures | Develop diversified investment portfolios and flexible financial structures to manage potential risks associated with international property investments. |

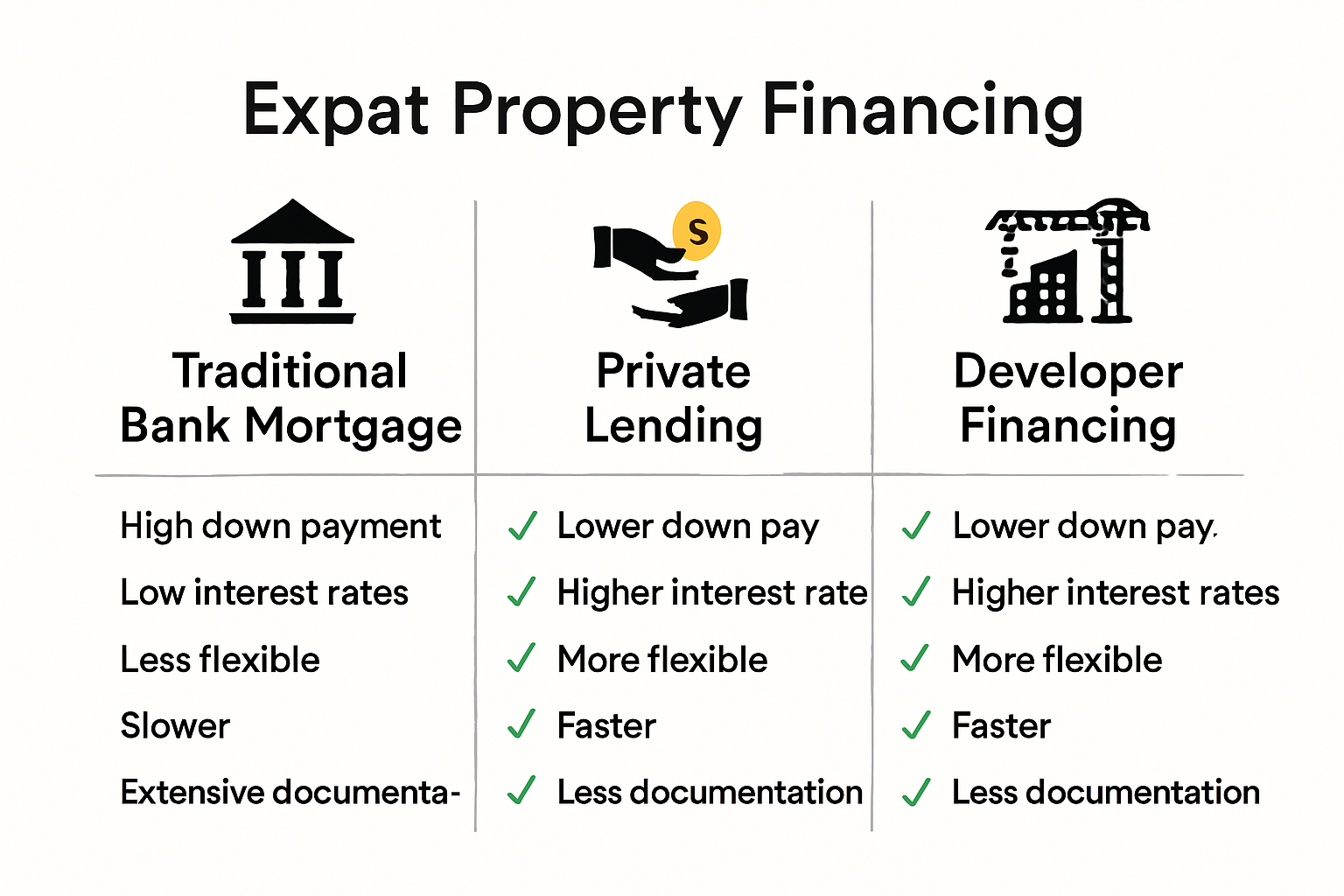

Key Expat Property Financing Options Explained

Expat property financing in 2025 demands strategic understanding of multiple funding approaches. Successful international property purchases require careful navigation through complex financial landscapes, with each financing option presenting unique advantages and potential challenges.

Traditional Banking Mortgage Solutions

Traditional bank mortgages represent the most established pathway for expat property financing. Local and international banks offer structured lending programs tailored to foreign property buyers. These mortgages typically require substantial documentation, including proof of income, credit history, and comprehensive financial statements.

Most banks demand higher down payments from expat borrowers – often ranging between 30% to 50% of the property’s total value. Interest rates for expat mortgages tend to be marginally higher compared to local resident rates, reflecting the perceived increased risk associated with international lending. Borrowers should anticipate thorough credit assessments and potentially stricter qualification criteria.

Key Mortgage Considerations:

- Credit Requirements: Strong international credit profiles are essential

- Down Payment: Higher percentage compared to domestic mortgages

- Documentation: Extensive financial verification process

Private Lending and Alternative Financing

Private lending emerges as a flexible alternative for expats seeking property financing. These specialized lending platforms offer more adaptable terms compared to traditional banking institutions. explore our flexible lending options for personalized property investment strategies.

Private lenders often provide faster approval processes and more lenient qualification standards. They specialize in understanding unique expat financial scenarios, considering factors beyond standard credit scores. Some private lending platforms focus specifically on real estate investments, offering tailored solutions that address the complex needs of international property buyers.

Advantages of private lending include:

- Faster Approval: Streamlined documentation processes

- Flexible Terms: Customized repayment structures

- Broader Qualification Criteria: Beyond traditional credit scoring

Developer Financing and Direct Investment Channels

Developer financing represents an increasingly popular option for expat property buyers. Many real estate developers now offer direct financing programs, allowing investors to purchase properties through structured payment plans. These arrangements can significantly reduce upfront capital requirements and provide more accessible entry points into international property markets.

Direct investment channels often include options like:

- Installment-based purchase agreements

- Phased payment structures

- Equity partnership models

Expats considering developer financing should conduct comprehensive due diligence. Carefully review contract terms, understand potential risks, and verify the developer’s reputation and track record in the specific market.

Successful expat property financing in 2025 requires a multi-dimensional approach. By understanding various funding strategies, international property buyers can make informed decisions that align with their financial goals and risk tolerance. Thorough research, professional consultation, and a strategic mindset remain crucial in navigating the complex world of international property investment.

Eligibility, Documentation, and Local Regulations

Navigating expat property financing requires a comprehensive understanding of eligibility criteria, documentation requirements, and intricate local regulations. Successful international property investments hinge on meticulous preparation and strategic financial planning.

Expat Financial Eligibility Criteria

Financial eligibility for expat property financing involves a complex evaluation of multiple factors. Lenders assess an individual’s financial stability through a comprehensive lens that extends beyond traditional credit scoring. Income verification becomes paramount, with institutions scrutinizing international earnings, employment stability, and overall financial health.

Key eligibility parameters typically include:

- Consistent Income Documentation: Minimum two years of stable international income

- Credit History: Strong international or U.S. credit profile

- Debt-to-Income Ratio: Generally restricted to 43% or lower

- Asset Reserves: Demonstrated ability to cover mortgage payments and additional expenses

Expats with complex financial backgrounds may face additional scrutiny. International professionals working for multinational corporations or those with diverse income streams must prepare extensive documentation to substantiate their financial standing. learn more about our comprehensive lending assessment for detailed insights into qualification processes.

Documentation Requirements for International Borrowers

Comprehensive documentation serves as the cornerstone of successful expat property financing. Lenders demand an extensive paper trail that validates financial credibility and mitigates potential risks associated with international lending.

Critical documents typically required include:

- Passport and Residency Verification: Proof of legal status and international identification

- Income Verification: Tax returns from home country and international employers

- Bank Statements: Comprehensive financial records demonstrating consistent cash flow

- Employment Verification: Official documentation confirming current employment and income stability

International borrowers must prepare translated and notarized documents that meet specific lender requirements. Some financial institutions specialize in expat lending and offer more flexible documentation guidelines, understanding the unique challenges faced by international professionals.

Navigating Local Regulatory Landscapes

Local regulations represent a critical consideration in expat property financing. Each jurisdiction maintains distinct legal frameworks governing property ownership and international investments. Regulatory environments can significantly impact financing options, tax implications, and overall investment viability.

Key regulatory considerations include:

- Foreign Investment Restrictions: Potential limitations on property ownership

- Tax Implications: Complex cross-border tax reporting requirements

- Legal Ownership Structures: Varying regulations concerning property title and ownership

Successful expat investors must collaborate with local legal experts and financial advisors who understand the intricate regulatory landscapes. Professional guidance helps navigate potential pitfalls and ensures compliance with local and international financial regulations.

Expat property financing in 2025 demands a strategic approach that balances financial preparedness with regulatory intelligence. Thorough research, meticulous documentation, and professional guidance remain essential for international property investors seeking to maximize their investment potential.

Maximizing Passive Income with Global Property

Passive income through global property investments represents a sophisticated strategy for expats seeking financial diversification and long-term wealth generation. Strategic property investment can transform real estate from a simple asset into a powerful income-producing mechanism.

Rental Property Investment Strategies

Rental property investments offer expats a robust pathway to generating consistent passive income. Successful strategies involve selecting properties in high-demand locations with strong rental potential. Target markets with robust economic indicators, growing populations, and emerging infrastructure developments.

Key considerations for rental property investments include:

- Location Selection: Areas with consistent job market growth

- Property Type: Multi-unit properties or apartments with higher income potential

- Occupancy Rate: Markets with sustained rental demand

Smart investors diversify their rental property portfolio across different geographic regions. explore our investment property recommendations to understand comprehensive global investment approaches. Professional property management becomes crucial for international investors, enabling seamless operations and maximizing rental income while minimizing personal management responsibilities.

Real Estate Investment Trusts and Passive Income Vehicles

Real Estate Investment Trusts (REITs) provide expats with an opportunity to generate passive income without direct property management. These investment vehicles allow individuals to invest in large-scale, income-producing real estate portfolios with significantly lower capital requirements compared to direct property ownership.

Advantages of REIT investments include:

- Liquidity: Easier buying and selling compared to physical properties

- Diversification: Exposure to multiple property types and geographic markets

- Professional Management: Experienced teams handling property operations

Investors can select from various REIT categories including residential, commercial, healthcare, and technology-focused real estate portfolios. Each category offers unique risk and return profiles, enabling strategic alignment with individual investment goals.

Strategic Partnership and Collaborative Investment Models

Collaborative investment models are emerging as powerful mechanisms for expats seeking to maximize passive income potential. These structures enable investors to pool resources, share risks, and access higher-value property investments that might be challenging to pursue individually.

Collaborative investment approaches include:

- Real Estate Syndications: Group investments in large commercial properties

- Fractional Property Ownership: Shared ownership with distributed income

- International Investment Consortiums: Cross-border investment partnerships

Successful collaborative investments require thorough due diligence, transparent legal frameworks, and aligned investment objectives. Investors must carefully evaluate potential partners, comprehend detailed investment agreements, and establish clear communication channels.

Maximizing passive income through global property demands a sophisticated, multifaceted approach. Successful expat investors combine strategic location selection, diverse investment vehicles, and innovative collaborative models. Continuous education, professional guidance, and adaptable investment strategies remain critical in navigating the complex global real estate landscape of 2025.

Common Challenges and Expert Solutions

Expat property financing in 2025 presents a complex landscape of intricate challenges that demand strategic navigation and innovative problem-solving. Understanding these obstacles and implementing expert-recommended solutions becomes critical for successful international property investments.

Financial and Credit Complexity

Expats frequently encounter significant financial hurdles that differentiate their investment journey from traditional property acquisition. International credit profiles often prove challenging, with many financial institutions maintaining stringent requirements that can effectively block potential investors from accessing mortgage products.

Primary financial challenges include:

- Credit History Limitations: Fragmented international credit records

- Income Verification Difficulties: Complex documentation requirements

- Currency Exchange Risks: Fluctuating international monetary landscapes

Mitigating these challenges requires a multifaceted approach. Investors must develop comprehensive financial portfolios that demonstrate stability across multiple jurisdictions. explore our specialized lending strategies for tailored international financing solutions that address these unique obstacles.

Legal and Regulatory Navigation

International property investments demand deep understanding of complex legal frameworks that vary dramatically across different jurisdictions. Regulatory environments can present substantial barriers, with each region maintaining distinct property ownership rules, tax implications, and foreign investment restrictions.

Key regulatory challenges encompass:

- Foreign Ownership Restrictions: Potential legal limitations on property acquisition

- Tax Compliance: Intricate cross-border reporting requirements

- Investment Structure Complexity: Varying legal frameworks for international investors

Successful navigation requires comprehensive legal consultation and strategic planning. Investors must develop robust networks of local legal experts who understand the nuanced regulatory landscapes of target investment regions.

Risk Mitigation and Strategic Planning

Effective risk management represents a critical component of successful expat property financing. Investors must develop sophisticated strategies that anticipate potential challenges and create flexible contingency plans.

Comprehensive risk mitigation strategies include:

- Diversified Investment Portfolios: Spreading risk across multiple property types and locations

- Comprehensive Insurance Coverage: Protecting investments against potential legal and financial uncertainties

- Adaptive Financial Structures: Flexible financing arrangements that accommodate changing market conditions

Professional investors recognize that successful international property financing extends beyond simple transaction completion. It requires a holistic approach that combines financial intelligence, legal expertise, and strategic foresight.

The landscape of expat property financing continues to evolve, demanding continuous learning and adaptability. Successful investors approach international property investments with a combination of thorough research, professional guidance, and flexible strategic thinking. By understanding potential challenges and developing comprehensive solutions, expats can transform complex financial obstacles into opportunities for significant wealth generation.

Frequently Asked Questions

What are the financing options available for expats in 2025?

Expat property financing options in 2025 include traditional banking mortgage solutions, private lending, and developer financing. Each option has its unique requirements and advantages, making it essential for expats to understand their various pathways.

How much down payment do banks require from expats?

In 2025, banks typically require expats to make down payments ranging from 30% to 50% of the property’s value, depending on the lender and the specific financing option.

What documentation is necessary for expats seeking property loans?

Expats need to provide extensive documentation, including proof of income, credit history, employment verification, bank statements, and identity verification, to meet lenders’ requirements and streamline the approval process.

How can expats maximize passive income through property investments?

Expats can maximize passive income by investing in rental properties located in high-demand areas, utilizing Real Estate Investment Trusts (REITs), or engaging in collaborative investment models to spread risk and increase income potential.

Ready to Overcome Expat Financing Barriers in Costa Rica?

If you are finding it tough to secure a mortgage with strict bank requirements, high down payments, or overwhelming documentation, you are not alone. The article above highlights how expats face unique challenges like high upfront costs and confusing regulations, especially when traditional banks say no. You need a smarter, faster solution to unlock property opportunities in Costa Rica.

Take control of your real estate goals now. Discover private lending options through CostaRicaLoanExperts.net that offer fast approvals, flexible terms, and transparent processes tailored for expats and investors. Whether you want a personalized loan or a high-yield property investment, our team helps you bypass the bank roadblocks so you can move forward with confidence. Explore our private lending solutions and connect with specialists today. Don’t let outdated lending stand in your way—start your smoother property journey today.