First lien loans are changing the way Costa Rica investors think about real estate financing. Most people picture these loans as a safety net for banks, but the real surprise is how much more they offer. Investors in Costa Rica can access up to 50 percent of their property value as capital while maintaining full ownership and legal control. That means you can tap into your property’s value for growth without selling a single share. The legal protections and strict documentation required in Costa Rica give lenders confidence, but it is the flexible access to capital and potential for steady passive income that really sets first lien loans apart.

Table of Contents

- What Are First Lien Loans And How Do They Work?

- Key Benefits For Property Owners And Investors

- First Lien Loans In Costa Rica: Unique Considerations

- How To Leverage First Lien Loans For Passive Income

Quick Summary

| Takeaway | Explanation |

|---|---|

| First lien loans provide enhanced security for lenders | These loans offer a primary legal claim on specific assets, reducing risk significantly for lenders, which in turn leads to more favorable terms for borrowers. |

| Investors maintain ownership while accessing capital | First lien loans allow property owners to leverage their assets for capital without diluting ownership or equity, enabling strategic deployment for growth opportunities. |

| Strict legal and regulatory framework in Costa Rica | Understanding the meticulous documentation and formal processes required for first lien loans in Costa Rica is crucial for securing financial interests in this market. |

| Potential for passive income generation | Investors can earn steady returns from first lien loans without active property management, making them a low-maintenance investment option with robust asset protection. |

| Key strategies include thorough due diligence | Successful investment in first lien loans requires careful evaluation of property quality and borrower credentials to mitigate risk and maximize passive income potential. |

What Are First Lien Loans and How Do They Work?

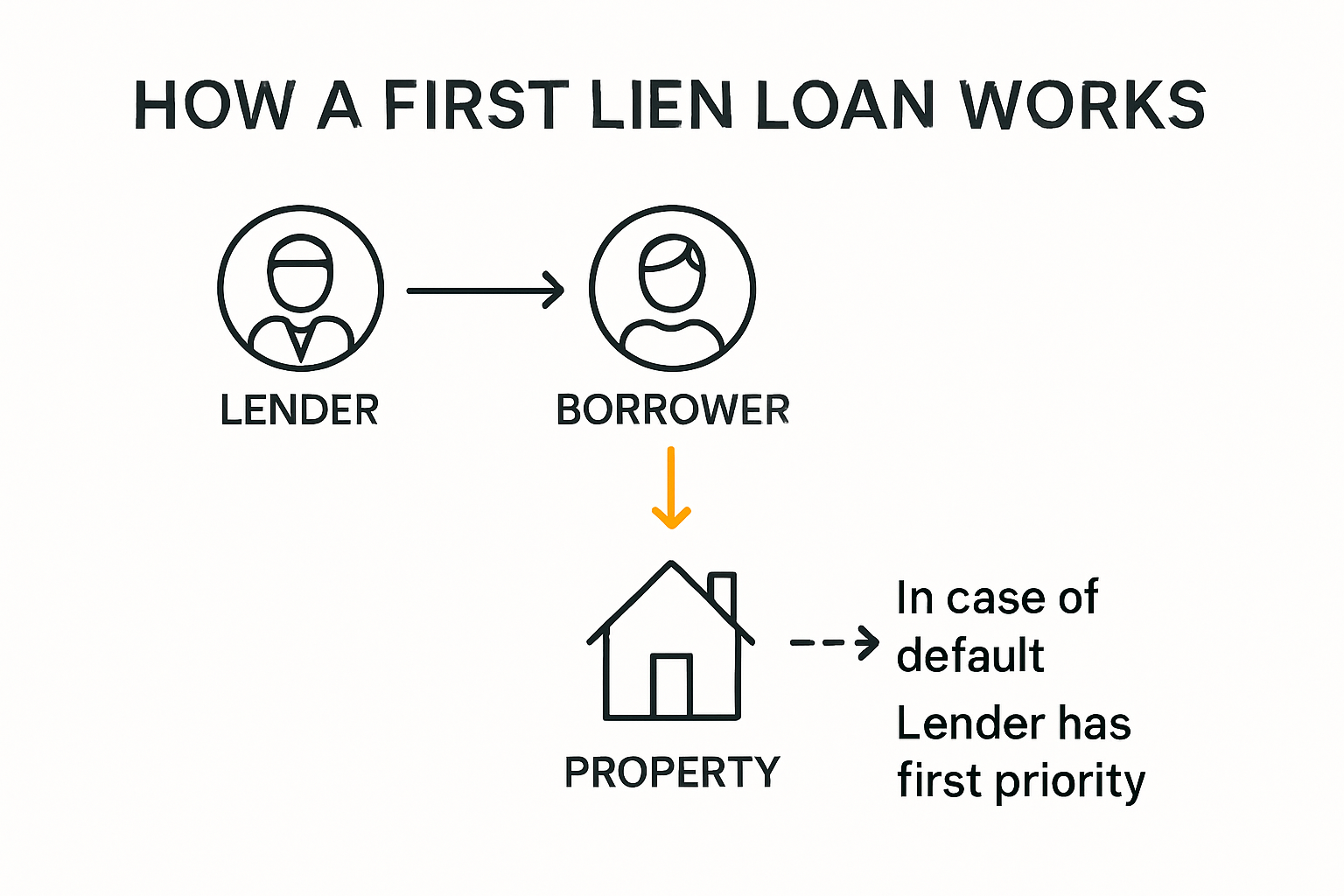

First lien loans represent a powerful financial instrument that provides secure lending options for real estate investors seeking strategic financial solutions. These specialized loans offer a unique approach to property financing by establishing a primary legal claim on specific collateral, creating a robust framework for both lenders and borrowers.

The Core Mechanics of First Lien Loans

At its fundamental level, a first lien loan gives the lender a primary legal position against a specific asset. When you secure a first lien loan, you are essentially creating a hierarchical structure of financial protection. Imagine this as a legal priority pass that ensures the first lien lender gets paid before any other creditors if the borrower encounters financial difficulties.

In the context of real estate investments, this means the lender has the first right to recover their investment by seizing and liquidating the pledged property. This priority status significantly reduces the risk for the lender, which translates into several key advantages for investors. First lien loans typically offer more favorable terms because the reduced risk allows lenders to provide more competitive interest rates and more flexible lending conditions.

Key Characteristics of First Lien Loan Structures

Understanding the structural nuances of first lien loans is crucial for investors. These loans come with several distinctive features that set them apart from traditional financing options. Collateral is the cornerstone of first lien lending, with the specific asset serving as a direct security mechanism. In real estate, this usually means the property itself becomes the primary guarantee for the loan.

The loan structure typically includes several critical components:

- Priority of Claim: The first lien lender has the highest ranking among potential creditors

- Asset Specificity: The loan is directly tied to a specific piece of real estate

- Risk Mitigation: Lower risk for lenders due to clear legal protections

When a borrower defaults on a first lien loan, the lender can initiate foreclosure proceedings and recover their investment directly from the property’s value. This process provides a clear and legally protected pathway for loan recovery, which is why many investors and private lenders find first lien loans an attractive investment vehicle.

For real estate investors in Costa Rica, first lien loans offer a sophisticated financing strategy that balances risk and opportunity. They provide a structured approach to property investment that allows for greater financial flexibility while maintaining strong legal protections for both lending parties. By understanding these loan mechanisms, investors can make more informed decisions about their real estate financing strategies, leveraging the unique advantages of first lien loan structures to maximize their investment potential.

Whether you are a seasoned investor or exploring real estate opportunities for the first time, first lien loans represent a strategic tool that can help you navigate the complex world of property financing with greater confidence and security.

Key Benefits for Property Owners and Investors

First lien loans provide a strategic financial tool that offers substantial advantages for property owners and investors in the real estate market. These specialized lending instruments create unique opportunities for capital acquisition, risk management, and investment growth, making them an attractive option for sophisticated financial planning.

Financial Flexibility and Capital Access

Property owners gain remarkable financial flexibility through first lien loans. Unlike traditional financing methods, these loans allow you to leverage your real estate assets without surrendering ownership or equity. This means you can access significant capital while maintaining complete control over your property investment. The loan structure enables property owners to unlock the inherent value of their real estate assets without complex restructuring or diluting their investment portfolio.

The capital accessed through first lien loans can be strategically deployed for various purposes. Investors might use these funds for property improvements, expanding their real estate portfolio, funding business operations, or seizing time sensitive investment opportunities. The versatility of first lien loans makes them an essential financial instrument for dynamic property investors who require quick and adaptable funding solutions.

Risk Mitigation and Lending Advantages

One of the most compelling benefits of first lien loans is the robust risk mitigation framework they provide. These loans offer superior protection for both lenders and borrowers through their unique legal positioning. For lenders, the first priority claim on collateral ensures a clear pathway to investment recovery. For borrowers, this translates into more favorable lending terms, including potentially lower interest rates and more flexible repayment structures.

The risk reduction mechanism inherent in first lien loans creates a win-win scenario. Lenders benefit from reduced financial exposure, while borrowers gain access to capital with more attractive conditions. This balanced approach makes first lien loans an intelligent choice for property investors seeking sophisticated financial strategies.

Key advantages include:

- Prioritized Collateral Recovery: First right to asset liquidation in default scenarios

- Lower Interest Rates: Reduced lending risk enables more competitive pricing

- Preservation of Ownership: Access to capital without equity dilution

For real estate investors in Costa Rica, first lien loans represent more than just a financing option. They are a strategic tool that enables precise financial maneuvering. By understanding and leveraging these loans, investors can optimize their property investments, manage risk effectively, and create sustainable growth pathways.

Whether you are expanding your real estate portfolio, seeking working capital, or looking to maximize the potential of your property assets, first lien loans offer a sophisticated approach to financial management. They provide a powerful mechanism for turning real estate holdings into dynamic, productive financial resources that can drive your investment strategy forward with confidence and strategic precision.

First Lien Loans in Costa Rica: Unique Considerations

Navigating the first lien loan landscape in Costa Rica requires a nuanced understanding of local legal frameworks, financial regulations, and unique market dynamics. Foreign investors and property owners must recognize that the Costa Rican lending environment presents distinct challenges and opportunities that differ significantly from other international real estate markets.

Legal and Regulatory Framework

Costa Rica’s approach to first lien loans is characterized by robust legal protections and a comprehensive regulatory system designed to safeguard both lenders and borrowers. Property transactions and loan agreements demand meticulous documentation and must be formalized through a notary public, creating an additional layer of legal verification that distinguishes Costa Rican lending practices. This process ensures that all first lien loan agreements are thoroughly vetted and legally binding.

The national registry plays a crucial role in establishing and protecting lien priorities. Investors must understand that proper registration is not just a formality but a critical step in securing their financial interests. This means that every first lien loan requires precise documentation that clearly establishes the lender’s primary claim on the underlying real estate asset. learn more about our specialized investor protections to understand the full scope of legal safeguards in place.

Financial Considerations and Market Dynamics

Unlike more liberal lending markets, Costa Rica maintains a conservative approach to property-backed financing. Investors should prepare for stringent qualification requirements and substantial down payment expectations. Typical first lien loans in Costa Rica often require down payments ranging from 30 to 50 percent of the property value, a significant consideration for investors accustomed to more lenient financing structures.

The unique financial landscape presents both challenges and opportunities. Interest rates and loan terms reflect the country’s measured approach to real estate lending. Foreign investors must be prepared for:

- Higher Initial Capital Requirements: Substantial down payment expectations

- Strict Verification Processes: Comprehensive documentation and background checks

- Currency Considerations: Potential fluctuations in exchange rates

Beyond financial mechanics, cultural nuances play a significant role in Costa Rican lending. Personal relationships, local market knowledge, and understanding regional economic variations become critical factors in successful first lien loan negotiations. Investors who approach these loans with patience, cultural sensitivity, and thorough preparation will find the most success.

The Costa Rican first lien loan market offers a sophisticated approach to real estate financing that prioritizes stability and legal protection. While the process may seem more complex compared to other international markets, it provides investors with a robust framework for secure property investments. This carefully regulated environment ensures that both lenders and borrowers have clear, legally protected pathways for their financial transactions.

For international investors, understanding these unique considerations is not just about navigating bureaucracy it is about recognizing the sophisticated financial ecosystem that makes Costa Rica an attractive destination for strategic real estate investments. Success requires more than capital it demands a deep appreciation for local legal and financial practices that protect all parties involved in the transaction.

How to Leverage First Lien Loans for Passive Income

Passive income strategies in real estate investment have evolved, with first lien loans emerging as a sophisticated method for generating consistent returns without active property management. These financial instruments offer investors a unique opportunity to earn steady income while maintaining robust asset protection and minimal operational involvement.

Understanding Passive Income Mechanics

First lien loans transform real estate investments into true passive income streams. Investors can generate monthly returns without directly managing properties, creating a hands-off approach to wealth generation. By providing capital secured against high-quality real estate assets, investors position themselves to receive predictable interest payments that require minimal ongoing effort.

The passive income model through first lien loans operates on a straightforward principle. When you invest in these loans, you become a private lender who receives regular interest payments based on the loan’s terms. Unlike traditional real estate investments that demand property maintenance, tenant management, or complex renovation projects, first lien loans offer a streamlined approach to generating investment returns. explore our comprehensive investor resources to understand the full potential of this investment strategy.

Strategic Investment Approaches

Successful passive income generation through first lien loans requires strategic planning and careful asset selection. Investors should focus on loans backed by high-quality real estate with strong market potential. This means evaluating properties in prime locations, assessing borrower credentials, and understanding the underlying asset’s intrinsic value.

Key strategies for maximizing passive income potential include:

- Diversification: Spread investments across multiple first lien loans

- Due Diligence: Thoroughly evaluate each loan’s underlying property and borrower

- Risk Management: Select loans with conservative loan-to-value ratios

The income potential of first lien loans is particularly attractive in markets like Costa Rica, where real estate continues to demonstrate resilience and growth. Investors can typically expect returns ranging from 8% to 12% annually, depending on the specific loan characteristics and market conditions. This return profile represents a compelling alternative to traditional investment vehicles like stocks or bonds.

Unlike other passive income strategies, first lien loans provide additional layers of security. The primary lien position means investors have the first claim on the underlying real estate asset in case of default. This structural advantage significantly mitigates investment risk and provides a robust safety mechanism that sets first lien loans apart from other passive income opportunities.

Successful passive income generation requires more than just capital. It demands a strategic approach that balances potential returns with comprehensive risk management. Investors who take the time to understand the nuanced mechanics of first lien loans position themselves to create sustainable, low-maintenance income streams that can support long-term financial goals.

Whether you are a seasoned investor seeking portfolio diversification or an individual looking to generate consistent passive income, first lien loans offer a sophisticated pathway to financial growth. By leveraging these specialized financial instruments, you can transform real estate assets into reliable, low-effort income generators that work continuously on your behalf.

Frequently Asked Questions

What are first lien loans?

First lien loans are a type of financing where the lender has the primary legal claim on a specific asset, such as real estate. This structure provides enhanced security for lenders and allows property owners to access capital while maintaining full ownership of their property.

How do first lien loans work in Costa Rica?

In Costa Rica, first lien loans require meticulous documentation and formal review through a notary public to establish the lender’s priority claim on the asset. These loans typically necessitate a substantial down payment of 30 to 50 percent of the property’s value, reflecting the country’s conservative lending environment.

What are the benefits of first lien loans for real estate investors?

First lien loans offer several advantages, including financial flexibility by allowing investors to access capital without equity dilution, lower interest rates due to reduced lender risk, and opportunities for passive income generation without the active management of properties.

How can I leverage first lien loans for passive income?

You can leverage first lien loans for passive income by investing in them as a private lender, securing predictable interest payments based on the loan terms without the need for property management. Focusing on high-quality real estate assets and thorough due diligence will maximize your potential returns.

Unlock the Full Power of First Lien Loans With Experts Who Know Costa Rica

Struggling to secure capital from traditional banks or worried about locking up your equity just to access funds? The article highlighted how first lien loans offer you a smarter route to financial flexibility and passive income while protecting your ownership rights and legal standing. The challenge is finding a trustworthy lender who understands Costa Rica’s complex legal environment and delivers fast, transparent service.

Experience what sets CostaRicaLoanExperts.net apart. Our platform specializes in connecting property owners and investors with vetted private lenders ready to offer well-structured, first-lien loans. Enjoy benefits like

- Quick approvals

- Clear, flexible terms

- Professional support for both borrowers and investors

Ready to unlock capital or start earning high, secure returns? Start your journey with our user-friendly loan request and investment tools now. The best opportunities in Costa Rica real estate move fast, so take action today and put the power of expertly structured, first-lien loans to work for you.