Property-backed loans are changing how expats and investors access money across borders. Imagine unlocking cash from your real estate without ever selling it. Think that is just for locals or people with perfect credit? Think again. In Costa Rica, foreign borrowers can qualify for loans worth up to 75 percent of a property’s appraised value, even if their credit history is from another country. Here is the surprising part. While the numbers sound impressive, the real story is in the doors this opens for global investors who used to get blocked at every bank. This new strategy flips the old rulebook. See how it works and why risk is only half the story.

Table of Contents

- What Are Property-Backed Loans And How Do They Work?

- Key Benefits For Expats And Real Estate Investors

- Risks And Requirements When Using Property As Collateral

- Steps To Get A Property-Backed Loan In Costa Rica

Quick Summary

| Takeaway | Explanation |

|---|---|

| Property-backed loans utilize real estate as collateral | These loans convert property from a passive asset to an active financial tool, allowing owners to access capital without selling their property. |

| Flexibility for expats and investors | Property-backed loans offer strategic advantages by bypassing traditional banking hurdles, making financing accessible without extensive local credit histories. |

| Importance of thorough documentation | Securing a property-backed loan requires meticulous legal and financial documentation, including clear titles and property values, which must often be translated and notarized for international borrowers. |

| Risk management is essential | Understanding the risks, such as foreclosure and market fluctuations, is crucial for borrowers, who should maintain financial buffers and insurance coverage to mitigate potential losses. |

| Navigating local requirements in Costa Rica is key | Investors must prepare comprehensive documentation and understand the local market for successful loan applications, which may take several weeks to months to process depending on complexity. |

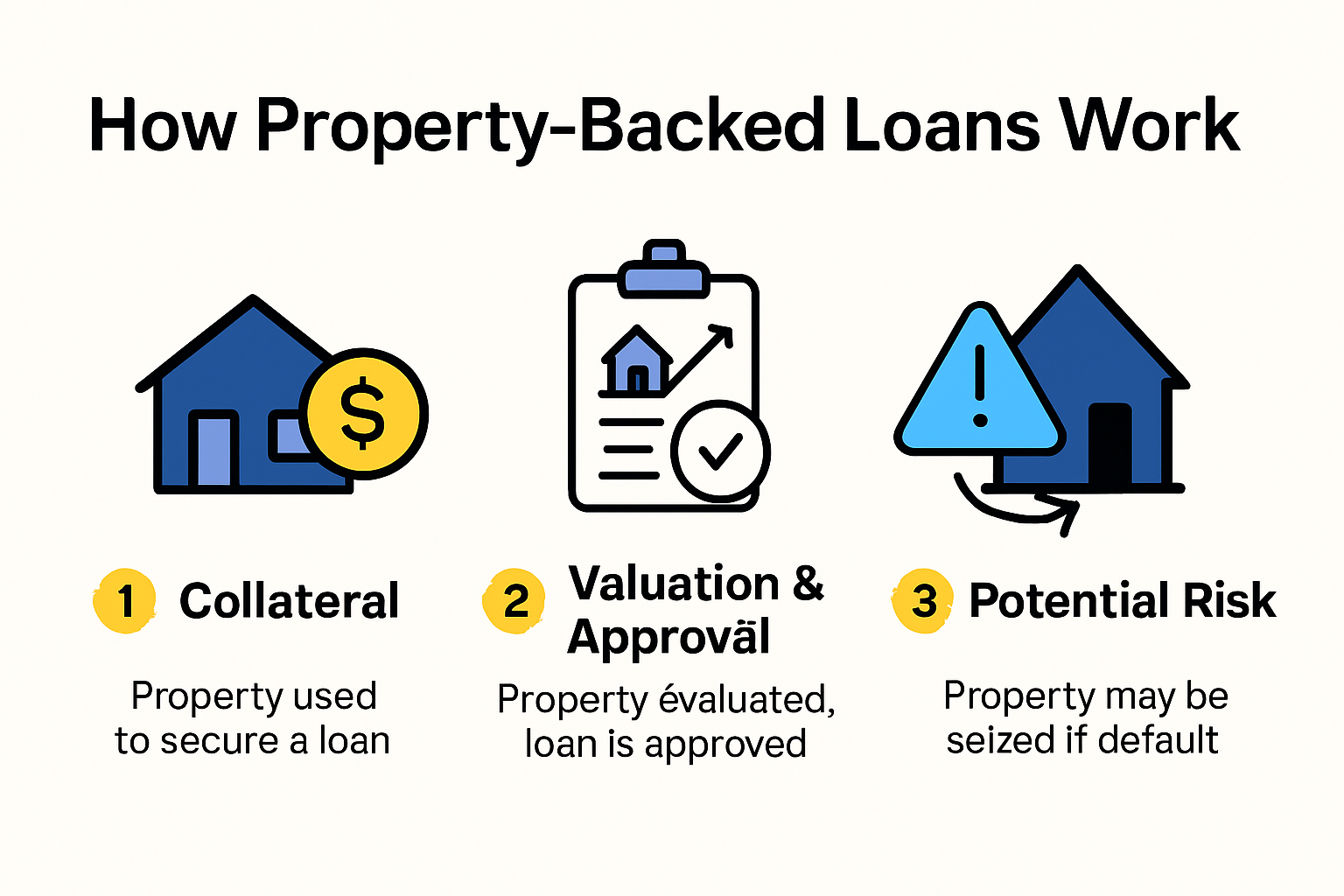

What Are Property-Backed Loans and How Do They Work?

Property-backed loans represent a powerful financial instrument where real estate serves as direct collateral, creating a secure lending mechanism that protects both borrowers and lenders. These specialized loans transform property from a passive asset into an active financial tool, enabling property owners to unlock their real estate’s monetary potential without selling.

The Core Mechanics of Property-Backed Lending

At its fundamental level, a property-backed loan transforms your real estate asset into a financial resource. When you secure a loan using your property, the lender establishes a legal claim against the real estate, which serves as security for the borrowed funds. This approach differs significantly from unsecured lending, where no specific asset guarantees repayment.

The valuation process becomes critical in property-backed loans. Lenders carefully assess the property’s market value, condition, location, and potential appreciation. They typically offer loan amounts ranging from 50% to 75% of the property’s current appraised value, creating a safety buffer that mitigates potential lending risks. This conservative approach protects the lender while providing borrowers access to substantial capital.

Risk Mitigation and Borrower Benefits

Property-backed loans offer unique advantages for investors and property owners. First lien position means the lender has primary claim on the property if default occurs, which reduces their risk and often translates to more favorable interest rates compared to unsecured financing options. For borrowers, this translates into predictable terms and potentially lower borrowing costs.

The flexibility of these loans makes them particularly attractive. Unlike traditional bank financing with rigid requirements, property-backed loans can accommodate diverse scenarios. Expats, international investors, and local property owners find these loans especially useful when conventional banking channels prove challenging. Whether you need capital for property improvements, business expansion, or personal investments, the property itself becomes the key qualification factor.

Understanding the mechanics is crucial. If a borrower fails to repay the loan, the lender can initiate foreclosure proceedings, selling the property to recover their invested funds. This structured approach provides clear pathways for both parties, reducing uncertainty and establishing transparent expectations from the outset.

The rise of private lending platforms has further transformed property-backed lending. These specialized services offer more personalized, faster approval processes compared to traditional banking institutions. They leverage technology and deep real estate market understanding to create efficient, transparent lending experiences that serve the unique needs of modern property investors and owners.

While property-backed loans offer significant opportunities, they require careful consideration. Borrowers must thoroughly understand loan terms, assess their repayment capabilities, and recognize the potential consequences of default. Professional consultation with lending experts who specialize in property-backed financing can provide invaluable guidance through this complex but potentially rewarding financial strategy.

Key Benefits for Expats and Real Estate Investors

Property-backed loans represent a strategic financial solution that offers transformative advantages for expats and real estate investors seeking flexible, intelligent capital deployment. These specialized lending instruments provide unique opportunities to leverage real estate assets in ways traditional financing cannot match.

Strategic Financial Flexibility

For expats and investors, property-backed loans unlock remarkable financial potential beyond conventional lending constraints. These loans fundamentally reimagine how real estate can generate value, allowing you to transform dormant property assets into dynamic financial resources. The core advantage lies in the loan’s structure: your property becomes more than just a physical asset. It evolves into a powerful financial tool capable of generating immediate capital without compromising ownership.

The lending landscape for international investors has dramatically transformed. Traditional banking systems often impose stringent requirements that exclude expats and foreign investors. Property-backed loans break through these barriers, offering a more inclusive approach. Instead of requiring extensive local credit history or complex documentation, these loans primarily evaluate the property’s inherent value and income potential. This approach means that even if you lack a domestic credit profile, you can still access substantial financing.

Investment Optimization and Risk Management

Low-risk investment strategy emerges as a standout benefit of property-backed loans. By using real estate as direct collateral, these loans provide a robust risk mitigation framework for both lenders and borrowers. Investors gain access to capital while maintaining a secure lending environment. The loan-to-value ratios typically range between 50% to 75%, creating a protective buffer that ensures lender security and borrower accountability.

The financial advantages extend beyond simple capital access. Property-backed loans enable sophisticated investors to optimize their portfolios through strategic leverage. You can acquire additional properties, fund renovations, or diversify investment streams without liquidating existing assets. This approach allows for dynamic portfolio management, where your real estate becomes an actively managed financial instrument rather than a passive holding.

For expats considering international real estate investments, these loans offer unprecedented geographical flexibility. Whether you’re looking to invest in residential properties, commercial real estate, or development projects, property-backed loans provide a standardized financing mechanism that transcends traditional geographical limitations. The ability to secure financing based on property value rather than personal credit history opens doors to global investment opportunities.

Investors recognize that property-backed loans represent more than just a financing method. They are a sophisticated financial strategy that transforms real estate from a static asset into a dynamic, income-generating resource. By understanding and leveraging these loans, you position yourself to maximize investment potential while maintaining robust risk management protocols.

Ultimately, success with property-backed loans requires thorough due diligence. Carefully evaluate loan terms, understand your repayment capabilities, and consult with financial professionals who specialize in international real estate financing. Your property is not just a piece of real estate. It is a strategic financial asset waiting to be optimized.

Risks and Requirements When Using Property as Collateral

Property-backed loans offer significant opportunities, but they also come with inherent risks and strict requirements that borrowers must carefully understand. Successfully navigating these financial instruments demands comprehensive knowledge of the potential challenges and precise documentation standards that lenders enforce.

Legal and Financial Documentation Standards

Securing a property-backed loan requires meticulous preparation of legal and financial documentation. Lenders conduct extensive due diligence to verify the property’s value, ownership status, and potential risks. You’ll need to provide comprehensive documentation including clear property titles, recent professional appraisals, detailed property condition reports, and proof of ownership. These documents must demonstrate unencumbered ownership and the property’s true market value.

International borrowers face additional scrutiny. Lenders often require translated and notarized documents, proof of legal residency, and verification of income sources. The documentation process can be complex, requiring patience and precise attention to detail. Some jurisdictions mandate specific legal certifications or translations, adding layers of complexity to the loan application process.

Potential Risks and Mitigation Strategies

Foreclosure risk stands as the most significant concern in property-backed lending. When you use your property as collateral, you essentially pledge the asset against loan repayment. Failure to meet loan obligations can result in property seizure. This risk underscores the critical importance of carefully assessing your financial capacity before securing a loan.

Property valuation presents another potential risk point. Market fluctuations can dramatically impact property values, potentially leaving borrowers with loans that exceed their property’s current market worth. Economic shifts, local market conditions, and unexpected development changes can rapidly alter property valuations. Savvy borrowers conduct independent property assessments and maintain financial buffers to protect against potential market downturns.

Legal complexities further compound the risks associated with property-backed loans. Different jurisdictions have varying regulations regarding property seizure, foreclosure processes, and borrower protections. International investors must navigate these intricate legal landscapes, understanding local laws that govern property lending and potential recourse mechanisms.

Risk mitigation requires a proactive approach. Borrowers should:

- Maintain comprehensive insurance coverage

- Create robust financial contingency plans

- Regularly assess property market conditions

- Maintain transparent communication with lenders

The loan-to-value ratio becomes a critical risk management tool. Most lenders limit financing to 50-75% of the property’s appraised value, creating a protective buffer against potential market fluctuations. This conservative approach protects both the lender and the borrower from excessive financial exposure.

Professional guidance becomes invaluable when considering property-backed loans. Financial advisors specializing in real estate lending can help you navigate complex documentation requirements, assess potential risks, and develop comprehensive strategies to protect your investment. Their expertise can mean the difference between a successful financial strategy and a potentially catastrophic lending experience.

Understanding these risks is not about discouragement but about informed decision-making. Property-backed loans remain a powerful financial tool when approached with knowledge, preparation, and strategic planning. Your property represents more than just collateral. It is a sophisticated financial asset that requires careful, intelligent management.

Steps to Get a Property-Backed Loan in Costa Rica

Securing a property-backed loan in Costa Rica requires strategic preparation and understanding of the local lending landscape. This process combines legal expertise, financial documentation, and careful navigation of the country’s unique real estate financing environment.

Initial Preparation and Documentation

Your journey begins with comprehensive preparation. You’ll need to assemble a detailed portfolio of documents that demonstrate your financial credibility and the property’s value. Essential documentation includes a valid passport, proof of stable income, comprehensive tax returns, translated bank statements, and a professional property appraisal. International investors must ensure all documents are officially translated into Spanish and notarized.

The property selection becomes a critical first step. Lenders will conduct thorough assessments of the real estate asset, evaluating its location, condition, market value, and potential for appreciation. Properties in prime areas with clear titles and no legal encumbrances stand the best chance of loan approval. Learn more about our investor financing options to understand how different property types impact loan eligibility.

Navigating the Application Process

Financial qualification represents a crucial phase in property-backed lending. Costa Rican lenders typically require more extensive documentation from foreign investors compared to local borrowers. Expect to provide proof of income from international sources, credit reports, and potentially demonstrate liquid assets that exceed the loan amount. Most lenders will require a down payment ranging from 30% to 50% of the property’s appraised value, creating a significant barrier for some investors.

The application process involves multiple stages of due diligence. Lenders will conduct comprehensive background checks, verify income sources, and assess the property’s legal status. This often involves working with local attorneys who specialize in real estate transactions. They will perform title searches, verify property boundaries, and ensure no outstanding legal issues could complicate the loan process.

Financial institutions in Costa Rica approach property-backed loans with significant caution. They prioritize risk mitigation through stringent evaluation processes. Your application will be scrutinized for:

- Comprehensive income documentation

- Clear property title

- Professional property appraisal

- Proof of legal residency or investment status

- Detailed financial history

The entire process can take several weeks to months, depending on the complexity of your application and the specific lender’s requirements. Patience and meticulous preparation become your greatest assets during this journey.

Successful loan acquisition requires more than just meeting technical requirements. Understanding the local real estate market, building relationships with local financial professionals, and demonstrating financial stability are crucial. Many expats and investors find that working with specialized lending platforms that understand the nuanced needs of international property investors can significantly streamline the process.

Ultimately, a property-backed loan in Costa Rica is more than a financial transaction. It represents an opportunity to leverage real estate assets in one of Central America’s most dynamic property markets. By approaching the process with thorough preparation, professional guidance, and a clear understanding of local requirements, you transform a complex financial journey into a strategic investment opportunity.

Frequently Asked Questions

What are property-backed loans?

Property-backed loans are financial instruments where real estate serves as collateral, allowing property owners to access capital without selling their property.

How do expats qualify for property-backed loans in Costa Rica?

In Costa Rica, foreign borrowers can qualify for loans worth up to 75% of a property’s appraised value, even without a local credit history.

What documentation is required for a property-backed loan?

Borrowers need clear property titles, recent appraisals, financial statements, proof of ownership, and for international investors, translated and notarized documents.

What are the risks associated with property-backed loans?

Potential risks include foreclosure if repayments are not met, and property valuation changes that can affect the loan-to-value ratio and overall borrowing capacity.

Ready to Unlock Capital in Costa Rica? Discover a Smarter Way to Borrow

Are you feeling held back by traditional banks that reject expats and international borrowers just because your credit history is not local? Property-backed loans let you turn your Costa Rican real estate into instant financial power. This article explained how private lending creates flexible options for expats and investors who need fast approvals and transparency, even when local banks say no.

Fast-track your next investment or secure working capital with confidence. Choose CostaRicaLoanExperts.net to connect directly with vetted private lenders who understand your unique needs and value your time. Our platform removes barriers and puts you in control. With our investor financing solutions, you can leverage your property or explore high-yield, real estate-backed returns in Costa Rica. Have questions or ready to act? Visit CostaRicaLoanExperts.net now and take the first step toward smarter, more flexible lending—before new opportunities pass you by.