Real estate loans are at the core of property investing for both locals and expats, and picking the right type can completely shape your financial future. But here is something most people miss. Some lenders in Costa Rica require down payments of up to 50 percent for foreign buyers, which is way higher than what many investors expect. This steep hurdle actually opens doors for creative financing ideas that most newcomers would never consider.

Table of Contents

- Types Of Real Estate Loans Explained

- How To Qualify For A Property Loan

- Understanding Loan Terms And Repayment

- Tips For Foreign And Local Investors In Costa Rica

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand loan types for investments | Different loans, like residential or commercial, affect financing options. Choose based on investment goals. |

| Prepare financial documentation thoroughly | Lenders require credit scores, income proof, and asset verification. Gather all necessary documents before applying. |

| Evaluate interest rates and repayment options | Analyze fixed vs. adjustable rates and repayment strategies to align with financial objectives and cash flow. |

| Research Costa Rican market dynamics | Understand local property laws, investment trends, and potential costs to create effective investment strategies. |

| Consult specialists for guidance | Work with financial and legal advisors familiar with real estate to navigate complexities and optimize decisions. |

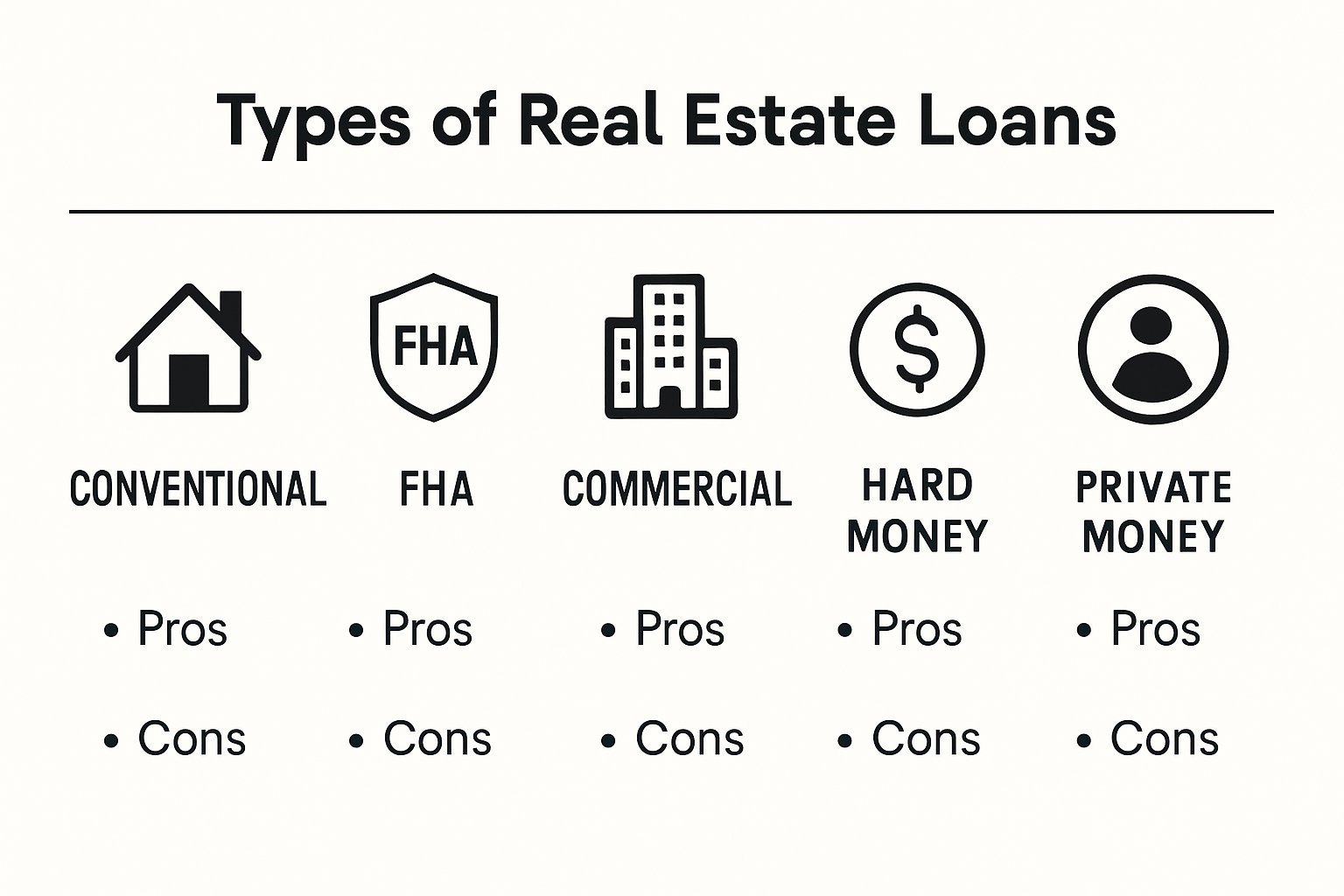

Types of Real Estate Loans Explained

Real estate loans represent a complex financial landscape with multiple financing strategies designed to meet diverse investor and property owner needs. Understanding the nuanced differences between loan types can significantly impact your investment success and financial planning.

To help you compare the main types of real estate loans mentioned, here is a summary of their key features and requirements:

| Loan Type | Typical Borrowers | Key Features | Typical Requirements |

|---|---|---|---|

| Conventional Loan | Residents, expats with strong credit | Fixed/adjustable rates, not government-backed | High credit score, solid income |

| Fixed-Rate Mortgage | Homeowners, individual investors | Predictable payments, rate locked for term | Proof of income, down payment |

| Adjustable-Rate Mortgage | Investors seeking initial low rates | Lower initial rate, may increase over time | Proof of income, good credit |

| FHA/Supported Loan | First-time buyers, moderate income | Lower down payment, more flexible standards | Lower credit/less cash, more documentation |

| Hard Money Loan | Investors needing fast funding | Short-term, property-based approval, flexible | High down payment, asset-based |

| Commercial Real Estate Loan | Investors in multi-unit/commercial | Evaluated by property income and market | Financials, income generation potential |

| Private Money/Alt. Financing | Investors with unconventional needs | Fast approval, flexible terms, less strict | Network or platform, variable terms |

Residential Real Estate Loans

Residential real estate loans form the foundation of property financing for individual investors and homeowners. These loans typically fall into several key categories that serve different financial profiles and objectives. Conventional loans represent the most common financing option, requiring solid credit scores and stable income documentation. These loans are not government-backed and often demand higher credit requirements compared to alternative financing methods.

Fixed-rate mortgages provide predictable monthly payments with interest rates locked for the entire loan term. Adjustable-rate mortgages offer initial lower rates that can fluctuate based on market conditions, potentially presenting both opportunities and risks for borrowers. Government-supported options like FHA loans enable lower down payment requirements and more flexible credit standards, making property ownership more accessible for first-time investors and those with moderate financial backgrounds.

Commercial and Investment Property Loans

Investment-focused real estate loans differ substantially from residential financing. These loans cater specifically to investors seeking to generate income through property acquisitions. Hard money loans emerge as a critical financing tool for investors requiring rapid funding and flexible approval processes. These short-term loans prioritize property value over traditional credit metrics, enabling faster transaction completion.

Commercial real estate loans support larger-scale investments in multi-unit residential properties, office spaces, retail locations, and industrial complexes. Lenders evaluate these loans based on potential income generation, property condition, and market positioning. Investors can access various structures including traditional bank financing, explore our specialized investment loan options designed for unique investment scenarios.

Private Money and Alternative Financing

Private money lending represents an increasingly popular real estate financing mechanism for investors seeking alternatives to traditional banking systems. These loans leverage personal networks, private investors, and specialized lending platforms to provide customized financing solutions. Private money loans often feature faster approvals, more flexible terms, and less stringent qualification requirements compared to conventional banking products.

Peer-to-peer lending platforms and self-directed investment accounts have expanded financing options for real estate investors. These innovative approaches allow individual investors to access funding directly from other private investors, bypassing traditional institutional lending constraints. Such alternative financing methods can offer competitive interest rates and more personalized lending experiences tailored to specific investment strategies.

Navigating real estate loan options requires comprehensive understanding of individual financial goals, risk tolerance, and specific investment objectives. Investors must carefully assess loan terms, interest rates, repayment structures, and potential long-term financial implications before selecting a financing strategy. Consulting with financial professionals who specialize in real estate investments can provide invaluable insights and guidance throughout the loan selection process.

How to Qualify for a Property Loan

Qualifying for a property loan requires strategic financial preparation and understanding of lender requirements. Investors and expats must navigate a complex landscape of documentation, credit evaluation, and financial assessment to secure real estate financing.

Below is a checklist-style summary table of typical requirements and steps to prepare for property loan qualification as discussed:

| Step/Requirement | Needed for Approval? | Notes |

|---|---|---|

| Strong credit score (>680) | Yes | Foreigners may need higher score or more documentation |

| Tax returns (recent years) | Yes | Used to demonstrate stable, verifiable income |

| Bank statements | Yes | Proves liquidity, assets, and income transfers |

| Proof of income | Yes | Could be employment, investments, or rental income |

| Debt-to-income ratio <43% | Yes | Standard for most institutions |

| Asset verification | Yes | Documented for down payment, reserves |

| Property appraisal/title docs | Yes | For collateral and legal due diligence |

| International documentation | Sometimes | For expats: may include translations, contracts, etc. |

Credit and Financial Documentation

Credit scores represent the foundational element of loan qualification. Lenders use these numerical representations to assess borrower reliability and potential risk. Most private and institutional lenders prefer credit scores above 680 for favorable loan terms. Foreign investors and expats might face additional scrutiny, requiring comprehensive financial documentation that demonstrates stable income and international financial credibility.

Financial documentation extends beyond credit scores. Lenders typically request comprehensive records including tax returns, bank statements, proof of income, and asset verification. Self-employed individuals and international investors must provide more extensive documentation to validate their financial standing. learn more about property-backed loan requirements for a deeper understanding of documentation standards.

Income and Debt Assessment

Loan qualification heavily depends on income stability and debt-to-income ratio. Lenders calculate this critical metric by dividing total monthly debt payments by gross monthly income. Most financial institutions prefer a debt-to-income ratio below 43%. Expats and international investors might need to demonstrate consistent income through international bank statements, employment contracts, or investment income verification.

Reliable income sources include consistent employment, investment returns, rental income, and verifiable international earnings. Lenders evaluate income sustainability and predictability. Foreign investors must often provide additional proof of income transferability and long-term financial stability. This might involve international tax documents, translated financial statements, and comprehensive income verification from multiple sources.

Down Payment and Collateral Requirements

Down payment requirements vary significantly between loan types and lender policies. Conventional loans typically demand 20-25% of the property’s total value, while specialized investor loans might offer more flexible terms. Expats and international investors should prepare for potentially higher down payment expectations due to perceived increased financial risk.

Real estate serves as primary collateral for most property loans. Lenders conduct thorough property evaluations to determine loan-to-value ratios. The property’s condition, location, market value, and potential income generation become critical factors in loan approval. Investors must provide comprehensive property appraisals, title documentation, and potential income projections to strengthen their loan application.

Successful loan qualification requires meticulous financial preparation. Potential borrowers should review their financial profile months before applying, addressing potential credit issues, organizing documentation, and developing a comprehensive financial narrative. Working with financial advisors specializing in international real estate investments can provide valuable guidance through complex qualification processes.

Understanding lender expectations and proactively addressing potential qualification challenges can significantly improve loan approval chances. Investors and expats must approach property loan applications with strategic planning, comprehensive documentation, and a clear demonstration of financial reliability.

Understanding Loan Terms and Repayment

Navigating loan terms and repayment structures represents a critical aspect of real estate investment strategy. Investors and expats must develop comprehensive understanding of complex financial agreements to make informed decisions and protect their long-term financial interests.

Interest Rates and Loan Structures

Interest rates form the cornerstone of loan financial dynamics. Fixed-rate loans provide predictable monthly payments with consistent interest percentages throughout the loan term. Adjustable-rate loans offer initial lower rates that can fluctuate based on market conditions, presenting both potential advantages and risks for borrowers. Investors must carefully analyze the long-term financial implications of each rate structure.

Loan terms typically range from 15 to 30 years, with each duration presenting unique financial considerations. Shorter loan terms generally feature higher monthly payments but lower total interest costs. Longer-term loans provide more manageable monthly payments but result in significantly higher total interest expenditure over the loan’s lifetime. Sophisticated investors often strategically select loan terms aligned with their specific investment objectives and cash flow projections.

Repayment Strategies and Structures

Repayment mechanisms vary widely across different loan types. Amortizing loans represent the most common structure, where monthly payments systematically reduce both principal and interest. In the early stages of these loans, a larger portion of each payment applies to interest, with progressively more funds directed toward principal reduction as the loan matures. explore our comprehensive guide to loan repayment strategies for deeper insights into optimization techniques.

Interest-only loan options provide alternative repayment structures particularly attractive to investors. These arrangements allow borrowers to pay only interest for a specified initial period, potentially creating more flexible short-term cash flow management. However, investors must carefully evaluate the long-term financial implications and potential balloon payment requirements associated with such loan structures.

Prepayment and Penalty Considerations

Loan agreements often include complex prepayment clauses that can significantly impact overall investment strategy. Some loans impose substantial penalties for early principal reduction or complete loan payoff. Investors must meticulously review these terms to understand potential financial restrictions and optimize their repayment approach.

Additional fees and charges can substantially modify the total loan cost. Origination fees, closing costs, and potential refinancing expenses represent critical financial considerations beyond standard interest rates. Sophisticated investors develop comprehensive financial models that account for these additional expenses, ensuring a holistic understanding of the true loan investment cost.

Successful real estate loan management requires continuous financial monitoring and proactive strategy adjustment. Investors should regularly reassess their loan terms, market conditions, and personal financial objectives. Maintaining flexibility and developing a deep understanding of loan mechanics can transform a standard financing arrangement into a strategic financial tool.

Comprehensive loan term understanding extends beyond mathematical calculations. It demands a nuanced approach that integrates financial knowledge, market awareness, and personal investment goals. Investors who approach loan agreements with strategic thinking and detailed analysis position themselves for more successful and sustainable real estate investment outcomes.

Tips for Foreign and Local Investors in Costa Rica

Investing in Costa Rican real estate presents unique opportunities and challenges for both local and international investors. Understanding the nuanced landscape of property investment requires strategic approach, comprehensive market knowledge, and careful financial planning.

Legal and Regulatory Considerations

Property ownership rights in Costa Rica provide robust protections for foreign investors. The country maintains an open investment environment where foreigners enjoy the same property rights as local citizens. No restrictions exist on foreign property ownership, making Costa Rica an attractive destination for international real estate investments. Investors must however navigate specific legal requirements and documentation processes that differ from their home countries.

Comprehensive due diligence becomes paramount when investing in Costa Rican real estate. This involves verifying property titles through the National Registry, confirming zoning regulations, and understanding local municipal requirements. Engaging local legal professionals who specialize in real estate transactions can provide critical insights and help investors avoid potential legal complications. discover comprehensive investment strategies that can maximize your real estate investment potential.

Financial Strategies and Financing Options

Financial preparation represents a critical component of successful real estate investment in Costa Rica. Local banking systems offer limited financing options for foreign investors, often requiring substantial down payments and presenting higher interest rates compared to international markets. Many international investors opt for alternative financing strategies, including leveraging assets from their home countries or utilizing specialized private lending platforms.

Investors should develop comprehensive financial models that account for additional costs beyond property purchase price. These include property transfer taxes, legal fees, potential renovation expenses, and ongoing maintenance costs. Understanding the total investment requirement helps investors create more accurate financial projections and mitigate unexpected financial challenges.

Market Analysis and Investment Considerations

Successful real estate investment in Costa Rica demands thorough market research and strategic positioning. Different regions offer varied investment potential, with coastal areas and emerging urban centers presenting distinct opportunities. Investors must evaluate factors such as tourism trends, infrastructure development, potential rental income, and long-term appreciation prospects.

Local market dynamics play a significant role in investment success. Costa Rica’s real estate market experiences fluctuations influenced by economic conditions, international investment trends, and regional development initiatives. Investors should develop networks with local real estate professionals, understand seasonal market variations, and remain adaptable to changing economic landscapes.

Navigating the Costa Rican real estate market requires a holistic approach that combines legal knowledge, financial strategy, and cultural understanding. Successful investors develop patience, build strong local relationships, and maintain flexibility in their investment approach. Thorough research, professional guidance, and a long-term perspective can transform potential challenges into profitable investment opportunities.

Whether you are a local investor seeking expansion or an international buyer exploring new markets, Costa Rica offers a dynamic and promising real estate investment landscape. By understanding the intricate details of property acquisition, financing, and market dynamics, investors can position themselves for sustainable and profitable real estate investments.

Frequently Asked Questions

What types of real estate loans are available for investors in Costa Rica?

There are several types of real estate loans available, including conventional loans, fixed-rate mortgages, adjustable-rate mortgages, FHA-supported loans, hard money loans, commercial real estate loans, and private money or alternative financing options. Each type caters to different investor needs and financial profiles.

How can expats qualify for a property loan in Costa Rica?

To qualify for a property loan, expats need to prepare strong financial documentation, including a good credit score (typically above 680), proof of income, tax returns, and bank statements. Additionally, lenders may require a down payment, satisfactory debt-to-income ratio, and property appraisal.

What are the down payment requirements for foreign investors in Costa Rica?

Down payment requirements for foreign investors can vary widely. Many lenders may demand down payments of up to 50 percent, which is often higher than expectations for local borrowers. It’s important for investors to confirm specific requirements with their lenders.

What are the legal considerations for foreign investors buying property in Costa Rica?

Foreign investors have the same property ownership rights as Costa Rican citizens, but they must navigate specific legal requirements, like verifying property titles and understanding local zoning regulations. It’s advisable to engage local legal professionals to guide through the process.

Take Control of Your Real Estate Financing with Experts Who Understand Your Needs

Traditional banks often set impossible hurdles for property investors and expats in Costa Rica. If you have read about hefty down payment requirements, restrictive approval criteria, or the struggle to find rapid financing in the article, you know how overwhelming the process can feel. High down payments and intense documentation requests can keep your real estate plans on hold, even when you have valuable property ready to leverage. Many borrowers and investors desire fast decisions, flexible loan terms, and a reliable resource that will not turn them away because they do not fit a standard bank profile.

Stop letting big banks shape your financial future. Connect with the CostaRicaLoanExperts.net team and discover how private lending can open doors where others have closed them. Our portal brings you direct access to detailed loan offerings designed for both expats and local investors. Secure collateral-backed lending with fast approvals, flexible structures, and fully transparent terms. Do not wait for another opportunity to pass you by.

Take the next step—visit CostaRicaLoanExperts.net now and see how easy it is to request funding or explore high-yield investment opportunities. Your real estate goals deserve a partner that understands the local market and specializes in real solutions for non-traditional borrowers.

Recommended

- Types of Real Estate Loans in Costa Rica: 2025 Guide for Expats & Investors – costaricaloanexperts.net

- types of real estate loans – costaricaloanexperts.net

- Borrowing Against Property in 2025: Guide for Investors and Expats – costaricaloanexperts.net

- Real Estate Backed Loans in Costa Rica: Guide for Expats & Investors 2025 – costaricaloanexperts.net

- What Is a Real Estate Lead? Guide for Agents and Teams 2025 – Lead Linker

- Real Estate in Probate: California Planning Guide for Wealthy Families 2025 – Law Office of Eric Ridley